Direct Labor Efficiency Variance Managerial Accounting

At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content.

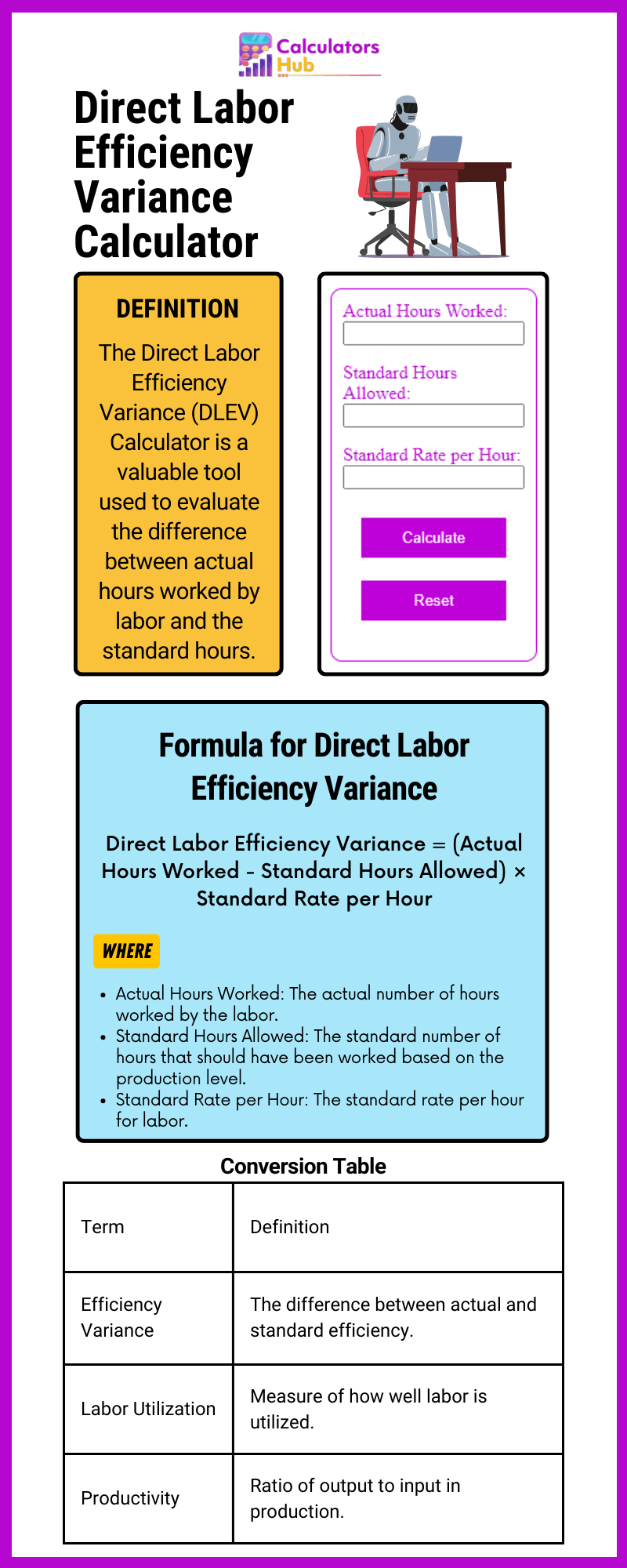

How to Calculate Direct Labor Efficiency Variance

This calculation will help you to compare the labor hours you’ve budgeted with the hours actually worked. By calculating it, you will pinpoint inefficiencies and make informed choosing a retirement plan 403b tax sheltered annuity plan decisions. Project deadlines are becoming tighter, and the rising cost of skilled labor, understanding and improving labor efficiency isn’t just a recommendation.

Causes of Unfavorable Labor Efficiency/Usage Variance:

Another element this company and others must consider is a direct labor time variance. On the other hand, if actual inputs are less than the amounts theoretically required, then there would be a positive efficiency variance. Since the baseline theoretical inputs are often calculated for the optimal conditions, a slightly negative efficiency variance is normally expected. The labor efficiency variance assesses the capacity to use labor in accordance with expectations. The variance can be used to draw attention to the portions of the production process that are taking longer than anticipated to finish.

Why is it important to calculate direct labor yield variance?

A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. Our mission is to empower readers with the most factual and reliable financial information possible to help them make informed decisions for their individual needs. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications. Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. Our team of reviewers are established professionals with decades of experience in areas of personal finance and hold many advanced degrees and certifications.

Suppose, for example, the standard time to manufacture a product is one hour but the product is completed in 1.15 hours, the variance in hours would be 0.15 hours – unfavorable. If the direct labor cost is $6.00 per hour, the variance in dollars would be $0.90 (0.15 hours × $6.00). For proper financial measurement, the variance is normally expressed in dollars rather than hours. Each bottle has a standard labor cost of \(1.5\) hours at \(\$35.00\) per hour. Calculate the labor rate variance, labor time variance, and total labor variance. Connie’s Candy paid \(\$1.50\) per hour more for labor than expected and used \(0.10\) hours more than expected to make one box of candy.

How Time Tracking Software Can Help Optimize Direct Labor Efficiency

A positive result indicates greater efficiency (i.e., less time was needed), while a negative result highlights inefficiencies (more time was used than planned). To arrive at the total cost per unit, we need to multiply the unit of material and labor with the standard rate. It is the estimated price of material and labor that a company need to pay to supplier and workers. The actual hours used can differ from the standard hours because of improved efficiencies in production, carelessness or inefficiencies in production, or poor estimation when creating the standard usage. Together with the price variance, the efficiency variance forms part of the total direct labor variance.

Insurance companies pay doctors according to a set schedule, so they set the labor standard. If the exam takes longer than expected, the doctor is not compensated for that extra time. Doctors know the standard and try to schedule accordingly so a variance does not exist.

- During the planning stages, the management staff might have projected that it will take 50 labor hours to produce one unit of a specific product.

- The direct labor variance measures how efficiently the company uses labor as well as how effective it is at pricing labor.

- When the job is finished, you find that you paid for 33 hours of labor at $60 per hour.

He has worked as an accountant and consultant for more than 25 years and has built financial models for all types of industries. He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own. He has been a manager and an auditor with Deloitte, a big 4 accountancy firm, and holds a degree from Loughborough University. If the balance is considered insignificant in relation to the size of the business, then it can simply be transferred to the cost of goods sold account. If this is not possible, the typical amount of time needed to make a good is increased to better reflect the degree of productivity.

If the actual rate of pay per hour is less than the standard rate of pay per hour, the variance will be a favorable variance. If, however, the actual rate of pay per hour is greater than the standard rate of pay per hour, the variance will be unfavorable. This shows that our labor costs are over budget, but that our employees are working faster than we expected. Even though the answer is a negative number, the variance is favorable because employees worked more efficiently, saving the organization money. What we have done is to isolate the cost savings from our employees working swiftly from the effects of paying them more or less than expected. This determination may stem from meticulous time and motion studies or negotiations with the employees’ union.

But on the other hand, if only 45 labor hours were actually used, then the efficiency variance would be +5, indicating that the manufacturing process was more productive and cost-effective than initially assumed. The labor efficiency variance is also known as the direct labor efficiency variance, and may sometimes be called (though less accurately) the labor variance. To put it simply, if your workers are taking longer to complete a task, your labor costs will go up.

The company does not want to see a significant variance even it is favorable or unfavorable. The actual results show that the packing department worked 2200 hours while 1000 kinds of cotton were packed. The direct labour total variance is the difference between what the output should have cost and what it did cost, in terms of labour. First, logistics have to maintain a steady stream of resources that are sufficient to keep workers from hitting stoppages. Secondly, hiring and training need to take labor efficiency into account.